AI Chip Quadrant Report

INTRODUCTION

AI chips are specialized hardware components designed to perform AI tasks efficiently. They are specifically tailored to handle the computational demands of AI workloads, such as machine learning algorithms, deep neural networks, and data-intensive processing. AI chips are built to accelerate the performance of AI tasks by optimizing key operations involved in AI computations, such as matrix multiplications, convolutions, and vector operations. AI chips leverage parallel processing techniques, advanced memory architectures, and specialized circuitry to deliver high-performance computing for AI applications. This chapter covers the drivers, restraints, opportunities, and challenges impacting the growth of the AI chip market. These factors help market players design strategies and devise action plans to grow and improve their performance in the market.

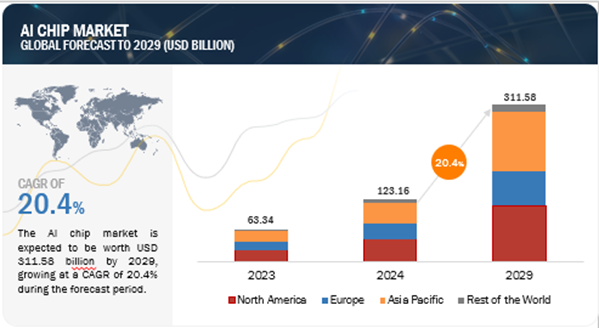

Attractive Opportunities in AI Chip Market

"During the forecast period, the GPU segment is anticipated to record the largest market share."

Over the duration of the projection period, the GPU category is anticipated to hold the greatest market share. The massive computational loads needed to train and execute deep learning models utilizing intricate matrix multiplications can be efficiently handled by GPUs. They are therefore essential in data centers and AI research, where effective hardware solutions are needed due to the rapid expansion of AI applications.

"Over the duration of the forecast period, the inference segment will take up the largest share of the AI chip market."

The market for AI chips with inference capabilities held the most share in 2023 and is anticipated to expand at the fastest rate over the course of the forecast period. Using pre-trained AI models, inference uses fresh data to generate quick judgments or precise forecasts. Strong inference skills in the data center are becoming more and more necessary as companies move toward AI integration to boost customer satisfaction, increase production efficiency, and spur creativity. Data centers are expanding their AI capabilities at a rapid pace, underscoring the significance of performance and efficiency in inference processing. The growing need for higher-performing and more energy-efficient inference chips is a key driver of the market expansion for AI chips. For example, SEMIFIVE has introduced their 14 nm AI Inference SoC Platform, which was created in partnership with South Korean company Mobilint, Inc. With a quad-core, high-performance 64-bit CPU, PCIe Gen4 interfaces, and LPDDR4 memory channels, this platform is specifically made for inference jobs. ASICs and other bespoke AI processors can use it. These chips are intended to enable big data analytics tools used for image and video recognition, data center accelerators, and AI vision processors. These techniques are all heavily dependent on scalable and effective inference processing. The growing need for specialized hardware solutions, which can aid in maximizing inference workload performance within data centers, is supported by the development of AI inference SoC platforms.

"During the forecast period, the generative AI segment will hold most of the market share."

The market for AI chips is anticipated to be dominated by generative AI technology for the projection. The demand for AI models that can provide high-quality text, image, and code content is growing exponentially. Data centre service providers strongly need AI chips with greater processing power and memory bandwidth as GenAI models get more complicated. Retail & e-commerce, BFSI, healthcare, media & entertainment, and dynamic applications like natural language processing, content creation, and automated design generation and process are just a few of the industries that are adopting GenAI applications at a remarkably high rate.

"During the forecast period, the cloud service providers segment is expected to hold the largest share of the AI chip market."

Over the duration of the forecast period, the cloud service providers (CSPs) sector is anticipated to hold the greatest share of the AI chip market. To remain competitive in the market, cloud service providers are progressively installing high-end AI chips in their data centers. For example, Northern Data Group (Germany) introduced Europe's first cloud services with NVIDIA's H200 GPUs in July 2024. The startup is expected to deliver an astounding 32 petaFLOPS of performance by utilizing 2,000 NVIDIA H200 GPUs. Throughout the projection period, the market for AI chips will expand thanks to these large investments made by CSPs.

"Asia Pacific is expected to increase at the fastest rate during the projection period."

Asia Pacific's AI chip market is expected to expand at the fastest rate throughout the projected period. Market expansion will be aided by the growing use of AI technology in nations like China, South Korea, India, and Japan. An atmosphere that is conducive to Al advancements is created by the substantial support that regional government organizations provide to AI research and development (R&D) operations. Further propelling the growth of the AI chip market in Asia Pacific over the coming years will be the presence of high-bandwidth memory (HBM) tech giants like Samsung (South Korea), Micron Technology Inc. (US), and SK Hynix Inc. (South Korea), which have dedicated HBM manufacturing facilities in South Korea, Taiwan, and China.

Key Market Players

Major vendors in the AI chip market are NVIDIA Corporation (US), Advanced Micro Devices, Inc. (US), Intel Corporation (US), Micron Technology, Inc. (US), Google (US), SK HYNIX INC. (South Korea), Qualcomm Technologies, Inc. (US), Samsung (South Korea), Huawei Technologies Co., Ltd. (China), Apple Inc. (US), Imagination Technologies (UK), Graphcore (UK), and Cerebras (US). Apart from this, Mythic (US), Kalray (France), Blaize (US), Groq, Inc. (US), HAILO TECHNOLOGIES LTD (Israel), GreenWaves Technologies (France), SiMa Technologies, Inc. (US), Kneron, Inc. (US), Rain Neuromorphics Inc. (US), Tenstorrent (Canada), SambaNova Systems, Inc. (US), Taalas (Canada), SAPEON Inc. (US), Rebellions Inc. (South Korea), Rivos Inc. (US), and Shanghai BiRen Technology Co., Ltd. (China) are among a few emerging companies in the AI chip market.

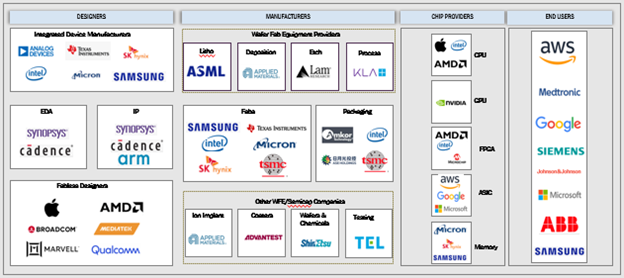

AI Chip Ecosystem

Source: MarketsandMarkets Analysis

Recent Developments

- In June 2024, Advanced Micro Devices, Inc. (US) introduced AMD Ryzen AI 300 Series processors with powerful NPUs offering 50 TOPS AI-processing power for next-generation AI PCs. These processors are powered by the new Zen5 architecture with 12 high-performance CPU cores and feature advanced AI architecture for gaming and productivity.

- In May 2024, Google (US) introduced Trillium, a sixth-generation TPU with improved training and serving times for AI workloads. It also has increased clock speed and the size of matrix multiply units. Trillium TPU powers the next wave of AI models.

- In April 2024, Micron Technology, Inc. (US) and Silvaco Group, Inc. (US) extended their partnership to develop an AI-based solution: Fab Technology Co-Optimization (FTCO). This solution enables customers to use manufacturing data to perform machine learning software simulations and create a computer model to simulate the wafer fabrication process. Micron Technology, Inc. (US) invested USD 5 million in the development of FTCO.

- In March 2024, NVIDIA Corporation (US) introduced the NVIDIA Blackwell platform to enable organizations to build and run real-time GenAI featuring six transformative technologies for accelerated computing. The platform allows AI training and real-time LLM inference for models with up to 10 trillion parameters.

- In February 2024, Intel Corporation (US) and Cadence Design Systems, Inc. (US) expanded their strategic partnership through a multiyear agreement to develop advanced system-on-chip (SoC) designs. The partnership aims to meet the rising demand from the fast-growing markets, including AI, ML, HPC, and premium mobile computing.

-

INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

2 MARKET OVERVIEW

2.1 INTRODUCTION

2.2 MARKET DYNAMICS

2.2.1 DRIVERS

2.2.1.1 Pressing need for large-scale data handling and real-time analytics

2.2.1.2 Rising adoption of autonomous vehicles

2.2.1.3 Surging use of GPUs and ASICs in AI servers

2.2.1.4 Continuous advancements in machine learning and deep learning technologies

2.2.1.5 Increasing penetration of AI servers

2.2.2 RESTRAINTS

2.2.2.1 Shortage of skilled workforce with technical know-how

2.2.2.2 Computational workloads and power consumption in AI Chip

2.2.2.3 Unreliability of AI algorithms

2.2.3 OPPORTUNITIES

2.2.3.1 Elevating demand for AI-based FPGA chips

2.2.3.2 Government initiatives to deploy AI-enabled defense systems

2.2.3.3 Rising trend of AI-driven diagnostics and treatments

2.2.3.4 Increasing investments in AI-enabled data centers by cloud service providers

2.2.3.5 Rise in adoption of AI-based ASIC technology

2.2.4 CHALLENGES

2.2.4.1 Data privacy concerns associated with AI platforms

2.2.4.2 Availability of limited structured data to develop efficient AI systems

2.2.4.3 Supply chain disruptions

2.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

2.4 PRICING ANALYSIS

2.4.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY COMPUTE

2.4.2 AVERAGE SELLING PRICE TREND, BY REGION

2.5 VALUE CHAIN ANALYSIS

2.6 ECOSYSTEM ANALYSIS

2.7 INVESTMENT AND FUNDING SCENARIO

2.8 CASE STUDY ANALYSIS

2.8.1 CDW INTEGRATED AMD EPYC SOLUTIONS TO ENSURE ENERGY EFFICIENCY AND OPTIMUM SPACE UTILIZATION

2.8.2 OVH SAS LEVERAGED AMD EPYC PROCESSOR TO OPTIMIZE PERFORMANCE OF CLOUD SOLUTIONS IN AI WORKLOADS

2.8.3 INTEL XEON SCALABLE PROCESSORS POWER TENCENT CLOUD’S XIAOWEI INTELLIGENT SPEECH AND VIDEO SERVICE ACCESS PLATFORM

2.8.4 AIC HELPS WESTERN DIGITAL TO ENHANCE SSD TESTING AND VALIDATION EFFICIENCY USING AMD PROCESSOR

3 COMPETITIVE LANDSCAPE

3.1 INTRODUCTION

3.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2019–2024

3.3 REVENUE ANALYSIS, 2021–2023

3.4 MARKET SHARE ANALYSIS, 2023

3.2 COMPANY VALUATION AND FINANCIAL METRICS

3.6 BRAND/PRODUCT COMPARISON

3.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

3.7.1 STARS

3.7.2 EMERGING LEADERS

3.7.3 PERVASIVE PLAYERS

3.7.4 PARTICIPANTS

3.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023

3.7.5.1 Company footprint

3.7.5.2 Compute footprint

3.7.5.3 Memory footprint

3.7.5.4 Network footprint

3.7.5.5 Technology footprint

3.7.5.6 Function footprint

3.7.5.7 End user footprint

3.7.5.8 Region footprint

3.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

3.8.1 PROGRESSIVE COMPANIES

3.8.2 RESPONSIVE COMPANIES

3.8.3 DYNAMIC COMPANIES

3.8.4 STARTING BLOCKS

3.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2023

3.8.5.1 Detailed list of key startups/SMEs

3.8.5.2 Competitive benchmarking of key startups/SMEs

3.9 COMPETITIVE SCENARIO

3.9.1 PRODUCT LAUNCHES

3.9.2 DEALS

4 COMPANY PROFILES

4.1 KEY PLAYERS

4.1.1 NVIDIA CORPORATION

4.1.1.1 Business overview

4.1.1.2 Products/Solutions/Services offered

4.1.1.3 Recent developments

4.1.1.3.1 Product launches

4.1.1.3.2 Deals

4.1.1.4 MnM view

4.1.1.4.1 Key strengths

4.1.1.4.2 Strategic choices

4.1.1.4.3 Weaknesses and competitive threats

4.1.2 ADVANCED MICRO DEVICES, INC.

4.1.2.1 Business overview

4.1.2.2 Products/Solutions/Services offered

4.1.2.3 Recent developments

4.1.2.3.1 Product launches

4.1.2.3.2 Deals

4.1.2.4 MnM view

4.1.2.4.1 Key strengths

4.1.2.4.2 Strategic choices

4.1.2.4.3 Weaknesses and competitive threats

4.1.3 INTEL CORPORATION

4.1.3.1 Business overview

4.1.3.2 Products/Solutions/Services offered

4.1.3.3 Recent developments

4.1.3.3.1 Product launches

4.1.3.3.2 Deals

4.1.3.3.3 Other developments

4.1.3.4 MnM view

4.1.3.4.1 Key strengths

4.1.3.4.2 Strategic choices

4.1.3.4.3 Weaknesses and competitive threats

4.1.4 SK HYNIX INC.

4.1.4.1 Business overview

4.1.4.2 Products/Solutions/Services offered

4.1.4.3 Recent developments

4.1.4.3.1 Product launches

4.1.4.3.2 Deals

4.1.4.3.3 Other developments

4.1.4.4 MnM view

4.1.4.4.1 Key strengths

4.1.4.4.2 Strategic choices

4.1.4.4.3 Weaknesses and competitive threats

4.1.5 SAMSUNG

4.1.2.1 Business overview

4.1.2.2 Products/Solutions/Services offered

4.1.2.3 Recent developments

4.1.2.3.1 Product launches

4.1.2.3.2 Deals

4.1.2.4 MnM view

4.1.2.4.1 Key strengths

4.1.2.4.2 Strategic choices

4.1.2.4.3 Weaknesses and competitive threats

4.1.6 MICRON TECHNOLOGY, INC.

4.1.6.1 Business overview

4.1.6.2 Products/Solutions/Services offered

4.1.6.3 Recent developments

4.1.6.3.1 Product launches

4.1.6.3.2 Deals

4.1.7 APPLE INC.

4.1.7.1 Business overview

4.1.7.2 Products/Solutions/Services offered

4.1.7.3 Recent developments

4.1.7.3.1 Product launches

4.1.7.3.2 Deals

4.1.8 QUALCOMM TECHNOLOGIES, INC.

4.1.8.1 Business overview

4.1.8.2 Products/Solutions/Services offered

4.1.8.3 Recent developments

4.1.8.3.1 Product launches

4.1.8.3.2 Deals

4.1.9 HUAWEI TECHNOLOGIES CO., LTD.

4.1.9.1 Business overview

4.1.9.2 Products/Solutions/Services offered

4.1.9.3 Recent developments

4.1.9.3.1 Product launches

4.1.9.3.2 Deals

4.1.10 GOOGLE

4.1.10.1 Business overview

4.1.10.2 Products/Solutions/Services offered

4.1.10.3 Recent developments

4.1.10.3.1 Product launches

4.1.10.3.2 Deals

4.1.11 AMAZON WEB SERVICES, INC.

4.1.11.1 Business overview

4.1.11.2 Products/Solutions/Services offered

4.1.11.3 Recent development

4.1.11.3.1 Product launches

4.1.11.3.2 Deals

4.1.12 TESLA

4.1.12.1 Business overview

4.1.12.2 Products/Solutions/Services offered

4.1.13 MICROSOFT

4.1.3.1 Business overview

4.1.3.2 Products/Solutions/Services offered

4.1.3.3 Recent developments

4.1.3.3.1 Product launches

4.1.3.3.2 Deals

4.1.14 META

4.1.4.1 Business overview

4.1.4.2 Products/Solutions/Services offered

4.1.4.3 Recent developments

4.1.4.3.1 Product launches

4.1.4.3.2 Deals

4.1.15 T-HEAD

4.1.12.1 Business overview

4.1.12.2 Products/Solutions/Services offered

4.1.16 IMAGINATION TECHNOLOGIES

4.1.16.1 Business overview

4.1.16.2 Products/Solutions/Services offered

4.1.16.3 Recent developments

4.1.16.3.1 Product launches

4.1.16.3.2 Deals

4.1.17 GRAPHCORE

4.1.17.1 Business overview

4.1.17.2 Products/Solutions/Services offered

4.1.17.3 Recent developments

4.1.17.3.1 Product launches

4.1.17.3.2 Deals

4.1.18 CEREBRAS

4.1.18.1 Business overview

4.1.18.2 Products/Solutions/Services offered

4.1.18.3 Recent developments

4.1.18.3.1 Product launches

4.1.18.3.2 Deals

4.2 OTHER PLAYERS

4.2.1 MYTHIC

4.2.2 KALRAY

4.2.3 BLAIZE

4.2.4 GROQ, INC.

4.2.5 HAILO TECHNOLOGIES LTD

4.2.6 GREENWAVES TECHNOLOGIES

4.2.7 SIMA TECHNOLOGIES, INC.

4.2.8 KNERON, INC.

4.2.9 RAIN NEUROMORPHICS INC.

4.2.10 TENSTORRENT

4.2.11 SAMBANOVA SYSTEMS, INC.

4.2.12 TAALAS

4.2.13 SAPEON INC.

4.2.14 REBELLIONS INC.

4.2.12 RIVOS INC.

4.2.16 SHANGHAI BIREN TECHNOLOGY CO., LTD.

COMPANY PROFILES

KEY PLAYERS

NVIDIA CORPORATION

ADVANCED MICRO DEVICES, INC

INTEL CORPORATION

SK HYNIX INC

SAMSUNG

MICRON TECHNOLOGY, INC

APPLE INC

QUALCOMM TECHNOLOGIES, INC

HUAWEI TECHNOLOGIES CO, LTD

GOOGLE

AMAZON WEB SERVICES, INC

TESLA

META

T-HEAD

IMAGINATION TECHNOLOGIES

GRAPHCORE

CEREBRAS

OTHER PLAYERS

MYTHIC

KALRAY

BLAIZE

GROQ, INC

HAILO TECHNOLOGIES LTD

GREENWAVES TECHNOLOGIES

SIMA TECHNOLOGIES, INC

KNERON, INC

RAIN NEUROMORPHICS INC

TENSTORRENT

SAMBANOVA SYSTEMS, INC

TAALAS

SAPEON INC

REBELLIONS INC

RIVOS INC

SHANGHAI BIREN TECHNOLOGY CO, LTD

- Updated version of this Quadrant

- Different Company Evaluation Quadrant

- 'Startup Only' Company Evaluation Quadrant

- Region or Country specific evaluation

- Application or Industry specific evaluation ..Read More

- Submit a Briefing Request

- Question about our published research

- Request for evaluation of your organization for specific market

- Request for re-evaluation of Company Evaluation Quadrant ..Read More